Hello friends, welcome to LoanOfferMe! If you have taken a home loan, here’s some fantastic news for you! Apart from the usual ₹2 lakh interest deduction (under Section 24b), you can also claim an additional deduction up to ₹1.5 lakh under Section 80EEA. This is specially designed for affordable housing loans. Let’s understand who can claim this and how.

Who is Eligible for 80EEA Deduction?

| Eligibility Criteria | Details |

| Applicant | Individual or Hindu Undivided Family (HUF) |

| Loan Sanction Date | Between 1st April 2019 to 31st March 2022 |

| Property Value | Up to ₹45 lakh (Stamp Duty Value) |

| Purpose | Purchase, construction or renovation of house |

| First-time Buyer | You should not own any residential property previously |

| Carpet Area (Metro Cities) | Not more than 60 square meters |

| Carpet Area (Other Cities) | Not more than 90 square meters |

How Much Deduction Can You Get?

Here’s how much deduction you get under different sections:

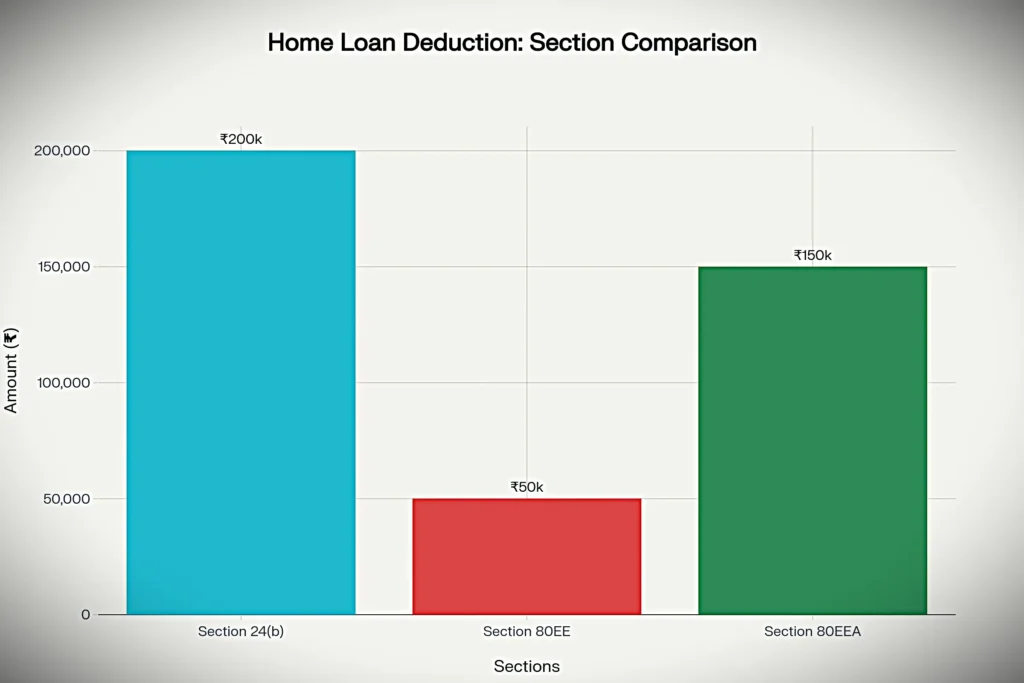

| Section | Maximum Deduction (₹) | For What |

| Section 24(b) | 2,00,000 | Home loan interest for self-occupied property |

| Section 80EEA | 1,50,000 | Additional interest for affordable housing |

Important Point: You can first claim ₹2 lakh under Section 24(b), then claim the remaining interest under Section 80EEA up to ₹1.5 lakh.

Tax Calculation with Real Examples

Case Study: Let’s assume you took a ₹30 lakh loan at 7% interest rate, with property value of ₹40 lakh.

| Scenario | Annual Interest | Section 24(b) | Section 80EEA | Total Deduction | Tax Saved (30% bracket) |

| Example 1 | ₹2,50,000 | ₹2,00,000 | ₹50,000 | ₹2,50,000 | ₹75,000 |

| Example 2 | ₹3,50,000 | ₹2,00,000 | ₹1,50,000 | ₹3,50,000 | ₹1,05,000 |

How to File in ITR – Step by Step Process

Step 1: First fill details in Section 24(b)

- Enter bank name, loan account number, sanction date correctly

- Claim maximum up to ₹2 lakh interest

Step 2: Then go to Section 80EEA section

- Fill the same loan details again (exactly same information)

- Claim the remaining interest amount (maximum up to ₹1.5 lakh)

⚠️ Warning: It’s essential to fill exact same loan details in both sections, otherwise you’ll get error in the portal.

80EE vs 80EEA Which is Better?

| Comparison Point | Section 80EE | Section 80EEA |

| Maximum Benefit | ₹50,000 | ₹1,50,000 |

| Property Value | Up to ₹50 lakh | Up to ₹45 lakh |

| Loan Period | 2016-2017 | 2019-2022 |

| Duration | Until loan is repaid | Maximum 5 years |

Important Points to Remember

- Old Tax Regime: This deduction is available only under old tax regime

- No Double Claiming: You cannot claim the same interest amount twice

- Joint Ownership: Husband-wife can claim separately if both are co-borrowers

- 5 Year Limit: This deduction is available for maximum 5 years from loan sanction

- First Home Only: Only first-time home buyers are eligible

If your property value is less than ₹45 lakh and loan was sanctioned after April 2019, you can take advantage of Section 80EEA. Combined with Section 24(b), you can get tax saving on total interest up to ₹3.5 lakh! Always keep your loan and property documents ready and fill correct details in ITR so there’s no problem in tax saving.

This guide gives you complete information about 80EEA deduction. If you’re planning home loan tax benefits this financial year, this information will be very useful for you! Thanks for reading, and don’t forget to visit LoanOfferMe.com for more such helpful content on loans and tax savings!

FAQs on Section 80EEA Home Loan Tax Deduction

What stamp duty value qualifies for 80EEA?

Only properties whose stamp duty value does not exceed ₹45 lakh are eligible for the 80EEA interest deduction.

What is the maximum interest I can claim under 80EEA?

You can claim up to ₹1.5 lakh per financial year as additional deduction on home loan interest under Section 80EEA.

Can I claim both Section 24(b) and 80EEA together?

Yes. First claim up to ₹2 lakh under Section 24(b) for self-occupied property, then claim the balance interest (up to ₹1.5 lakh) under Section 80EEA.

Will the online ITR portal show an error if details mismatch?

Yes. Make sure to enter exactly the same bank name, loan account number, sanction date, and loan amount in both sections to avoid portal warnings.

How many years is 80EEA deduction available?

You can claim Section 80EEA deduction for a maximum of five consecutive years from the loan sanction date.